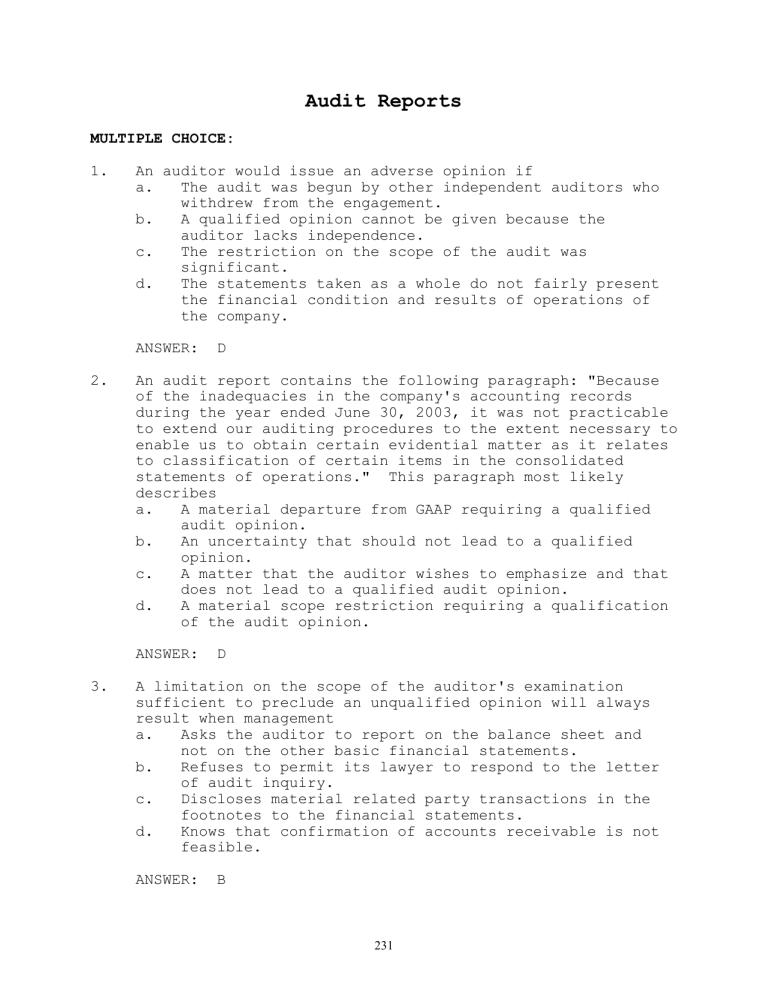

An Auditor Would Issue an Adverse Opinion if

There are three types of modification. Also the sales amount of USD 50000000 equal to 10 of total sales during the years has not occurred.

4 Types Of Audit Opinion Accounting Hub

The auditor expresses an adverse opinion when the auditor having obtained sufficient appropriate audit evidence concludes that misstatements individually or in the aggregate are both material and pervasive to the financial statements.

. The auditors report is recorded in the annual report the auditors report tests to see that a corporations financial statements comply with GAAP. Yet adverse opinion misstatements are both material and pervasive. Adverse Report Auditor gives negative reports based on examination of financial statements and evidence obtained.

An adverse opinion can damage a companys reputation and even have legal ramifications unless the issues are corrected. If the auditor is unable to determine the effect of the subsequent event on the effectiveness of ICFR the auditor should. The possible effects of undetected misstatements arising from an inability to obtain.

As per Section 193 of the Act the Governor of a State or the Administrator of a Union Territory having a legislative assembly may where he is of the opinion that it is necessary in the public interest so to do request the Comptroller and Auditor General to audit the accounts of a corporation established by law made by the legislature of the State or of the Union Territory as. For example the auditor concludes that the inventories amount to USD 500000 equal to 20 of total assets at the end of the year does not exist. Types of Modified Opinions 2.

They believe there is a material misstatement in the financial information that can affect stakeholders decisions. The disclaimer of opinion. The term of seriousness the qualified audit.

If the auditor concludes after consideration of managements plans that substantial doubt about the companys ability to continue as a going concern is alleviated the basis for the auditors conclusion including elements the auditor identified within managements plans that are significant to overcoming the adverse effects of the conditions and events. In these circumstances the auditor has to issue a modified version of their opinion. When the auditor expresses an adverse opinion the auditor shall state that in the auditors opinion because of the significance of the matters described in the Basis for Adverse Opinion section.

In this case the auditor issue a qualified audit opinion on the qualified audit report. An adverse opinion means that the misstatements in the financial statements are both material and pervasive. If the auditor obtains knowledge about subsequent events that materially and adversely affect the effectiveness of the companys ICFR as of the date specified in the assessment the auditor should issue an adverse opinion on ICFR.

In the independent auditors report an auditor can issue one of five different opinions. 42 When the auditor expresses an adverse opinion he or she should disclose in a separate paragraphs immediately following the opinion paragraph of the report a all the substantive reasons for his or her adverse opinion and b the principal effects of the subject matter of the adverse opinion on financial position results of operations and cash flows if. A private citizen cannot get an advisory ruling from a court and can only get rulings in an actual lawsuit.

This ISA also deals with how the form and content of the auditors. The audit reports of Deloitte on the Companys consolidated financial statements for the years ended December 31 2019 and December 31 2020 did not contain an adverse opinion or a disclaimer of opinion and were not qualified or modified as to uncertainty audit scope or accounting principles. A GAAP departure or a scope limitation.

The CARO 2020 will not apply to the auditors report on consolidated financial statements except for clause xxi of Clause 3 in regard to any qualifications or adverse remarks by the respective auditors in the Companies Auditors Report Order CARO reports of the companies included in the consolidated financial statements. There are two types of reservations that can be made. This ISA establishes three types of modified.

This International Standard on Auditing ISA deals with the auditors responsibility to issue an appropriate report in circumstances when in forming an opinion in accordance with ISA 700 Revised1 the auditor concludes that a modification to the auditors opinion on the financial statements is necessary. Disclaimer Report When the auditors cannot form an opinion on financial statements in the absence of sufficient and appropriate audit evidence. A When reporting in accordance with a.

An advisory opinion has no force of law but is given as a matter of courtesy. In this kind of report only inventories that mention are matter. Other financial information in the financial statements is true and fair.

However if the auditor thinks that the misstatement is pervasive they will issue an adverse opinion in their report. An adverse opinion on an audit report is the worst possible report that you can get. An adverse opinion is one of the four main types of opinions that an auditor can issue.

An opinion stated by a judge or a court upon the request of a legislative body or government agency. There are four types of audit reports. If there is any such remark then.

The other three are unqualified opinion which means that financial statements are presented in accordance. This International Standard on Auditing ISA deals with the auditors responsibility to issue an appropriate report in circumstances when in forming an opinion in accordance with ISA 7001 the auditor concludes that a modification to the auditors opinion on the financial statements is necessary. The opinion issued depends on the type of reservation which depends upon 1.

Their use depends upon the nature and severity of the matter under consideration. And unqualified opinion a qualified opinion and adverse opinion and a disclaimer of opinion. There are two factors that cause auditors to.

Guidance as to the usage of the three forms of modification is provided by ISA 705. The auditor disclaims an opinion when either. There are chances that the.

What Are Audit Opinions 4 Types Of Audit Opinions Explained With Example Audithow

Ch14 Audit Reports

Modified Audit Opinions

No comments for "An Auditor Would Issue an Adverse Opinion if"

Post a Comment